3 forces driving innovation in enterprise Networks

https://youtu.be/SKLKD3wdAfAWhat are the 3 biggest forces driving innovation in enterprise networks today? Cost, Cloud, and Connectivity, answered Shekar Ayar, CEO ...

https://youtu.be/SKLKD3wdAfAWhat are the 3 biggest forces driving innovation in enterprise networks today? Cost, Cloud, and Connectivity, answered Shekar Ayar, CEO ...

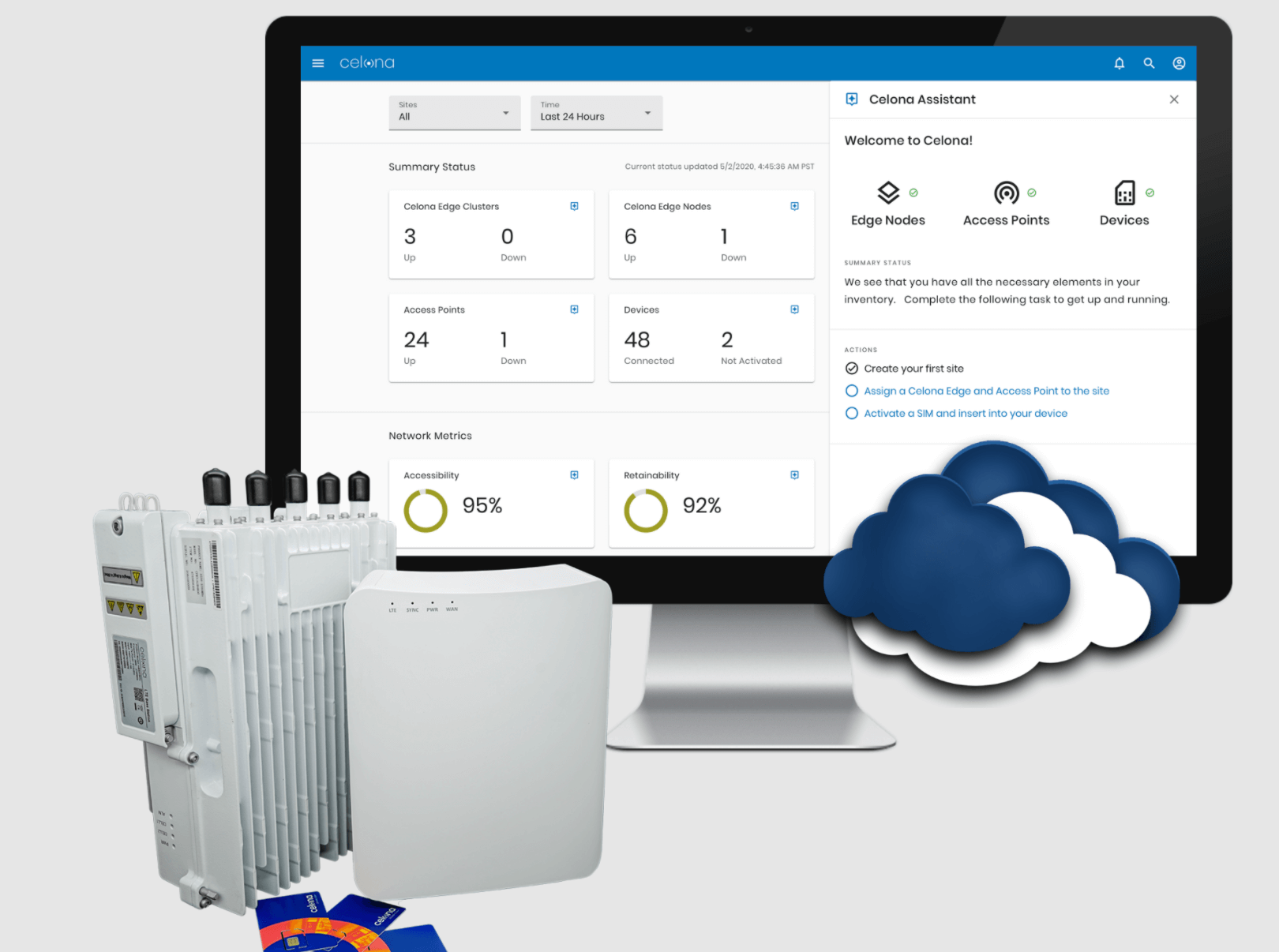

Celona, a start-up based in Cupertino, California, closed a $60 million Series C financing round for its solutions aimed at ...

Fortinet agreed to acquire AccelOps, a start-up based in Santa Clara, California, that specializes in network security monitoring and analytics ...

KT and Nokia announced the industry's first eMTC field trial, marking an important milestone for the Internet of Things, allowing ...

A private dossier for networking and telecoms