Angola Cables upgrades MONET subsea cable with Ciena

Angola Cables has upgraded its MONET submarine cable network using Ciena’s (NYSE: CIEN) GeoMesh, powered by WaveLogic Ai coherent optical ...

Angola Cables has upgraded its MONET submarine cable network using Ciena’s (NYSE: CIEN) GeoMesh, powered by WaveLogic Ai coherent optical ...

AWS will begin offering EC2 instances with up to eight of Intel's Habana Gaudi accelerators for machine learning workloads.Gaudi accelerators ...

Intel has acquired Habana Labs, an Israel-based developer of programmable deep learning accelerators for the data center, for approximately $2 ...

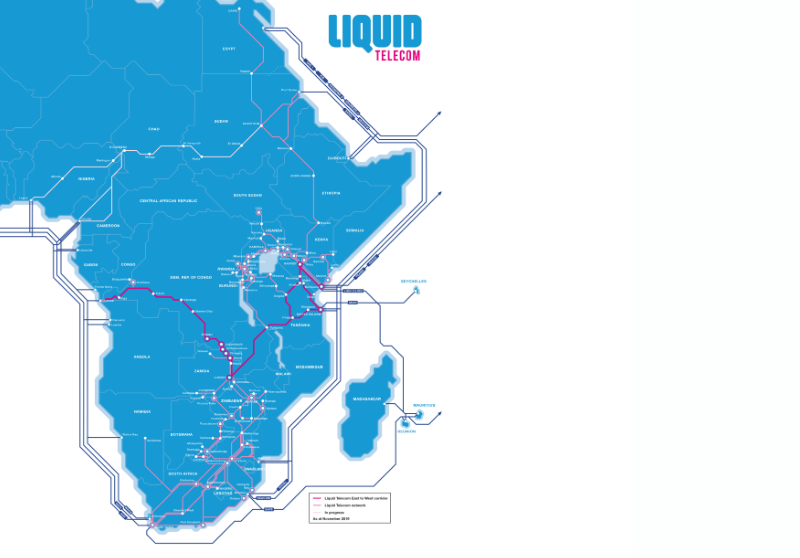

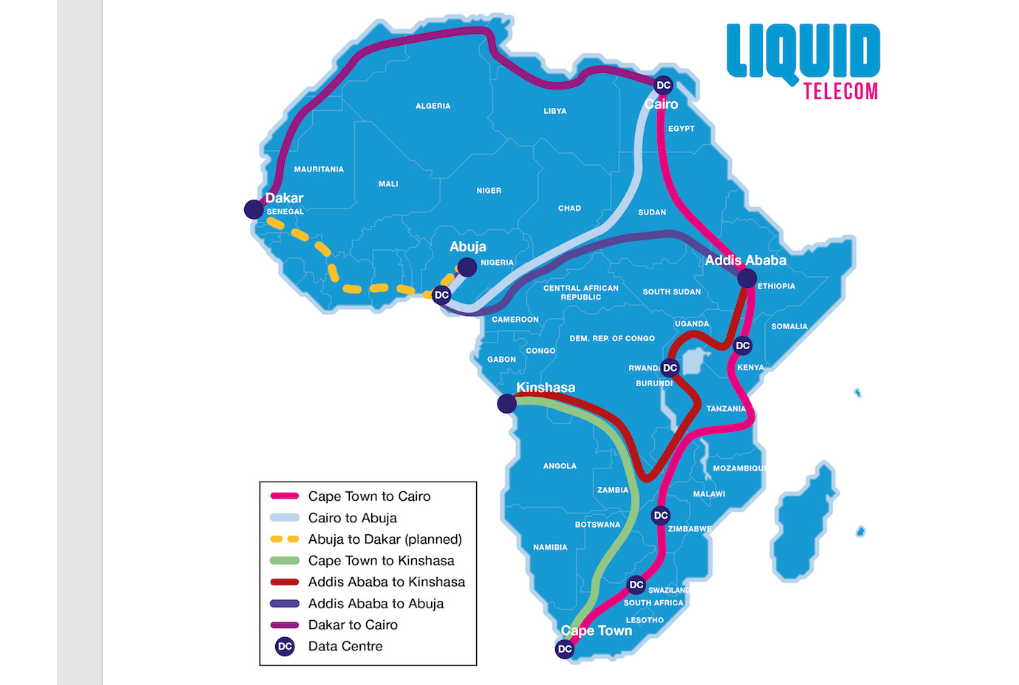

Liquid Telecom has launched a land-based fiber network connecting East to West Africa. The coast-to-coast digital corridor follows the completion ...

Rakuten Mobile has selected NEC to build its 5G open vRAN infrastructure in Japan. Through the partnership, Rakuten and NEC ...

Liquid Telecom will invest 8 billion Egyptian Pounds (US$400 million) in Egypt over the next three years as part of ...

The world’s first optical modules compliant with Consortium for On-Board Optics (COBO) will be shown at next week's ECOC Exhibition ...

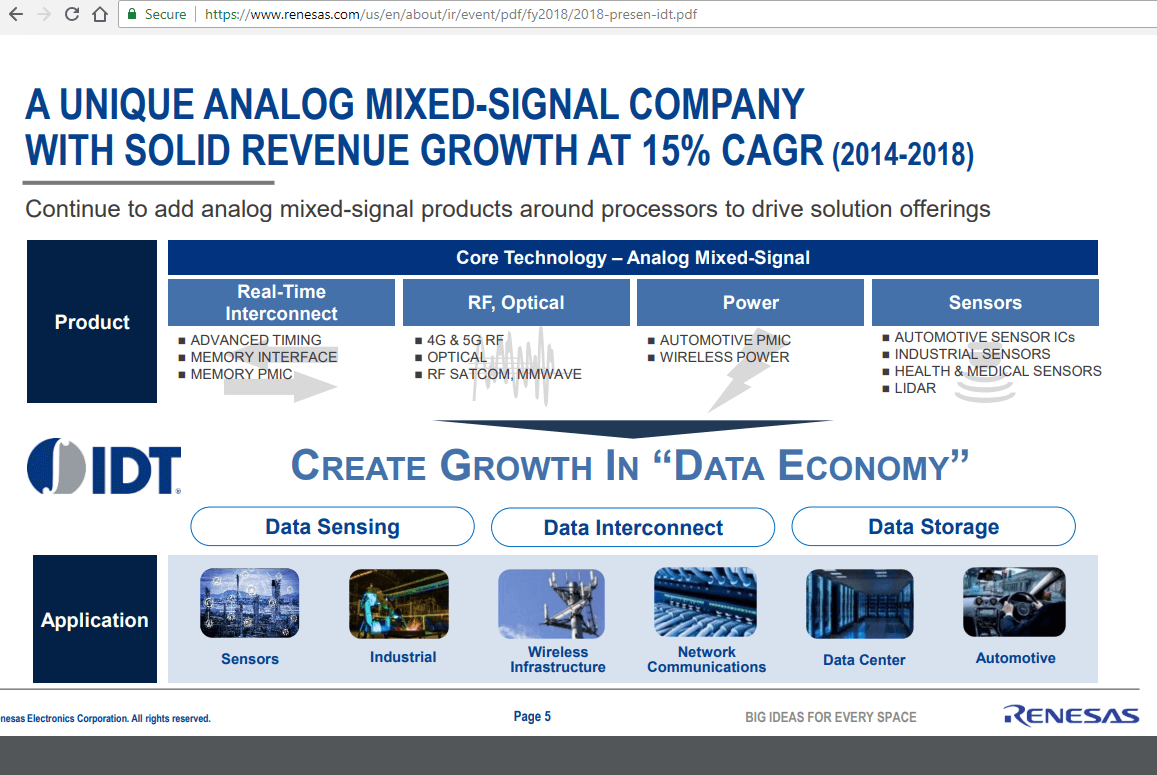

Renesas Electronics Corporation of Japan has agreed to acquire Integrated Device Technology (IDT, NASDAQ: IDTI) for approximately US$6.7 billion (approximately ...

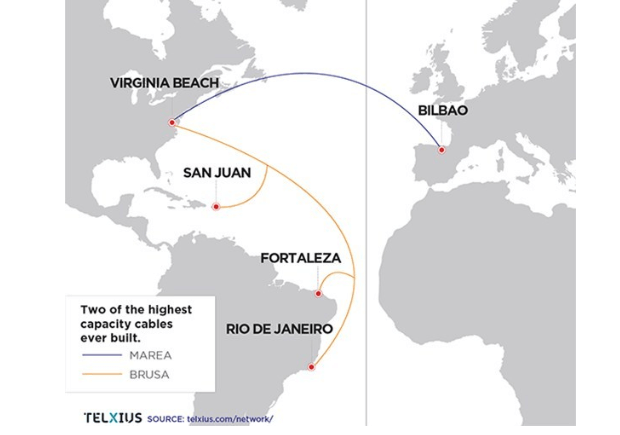

Telefónica will sell a 9.99% equity stake in Telxius, its infrastructure arm, to Pontegadea for a total of 378.8 million ...

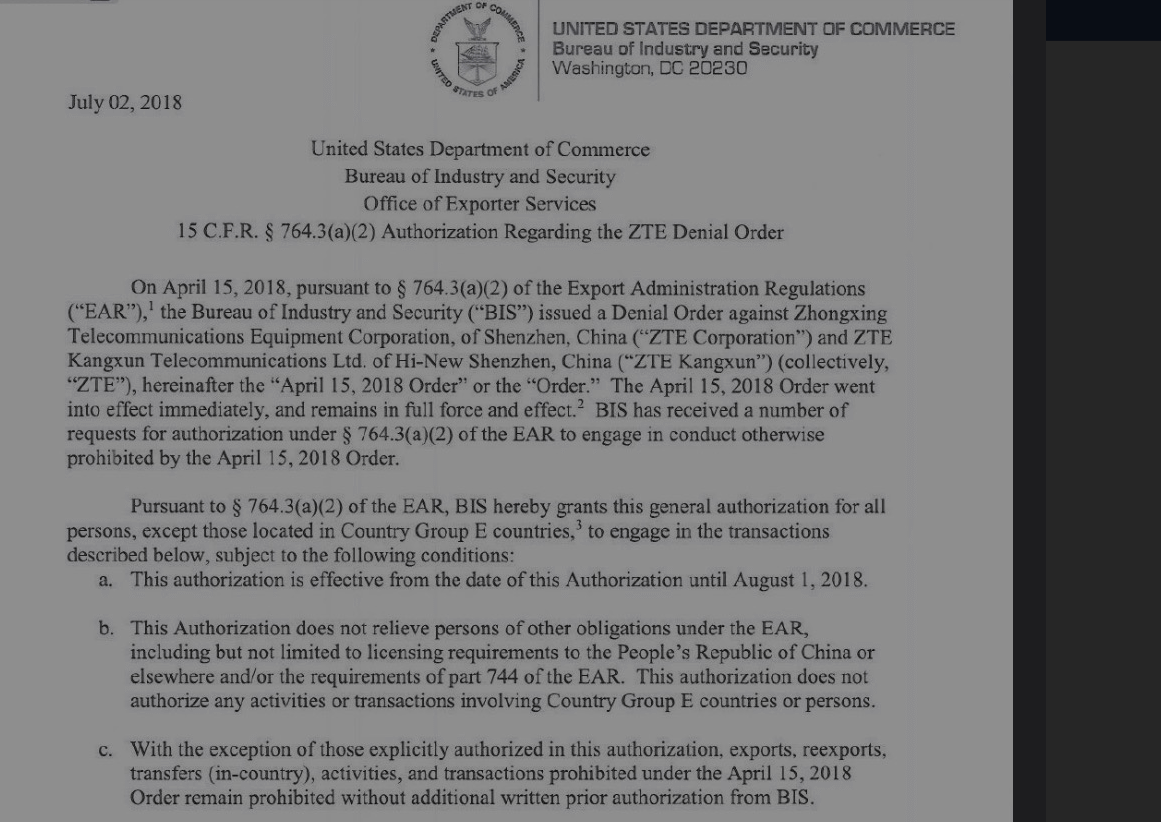

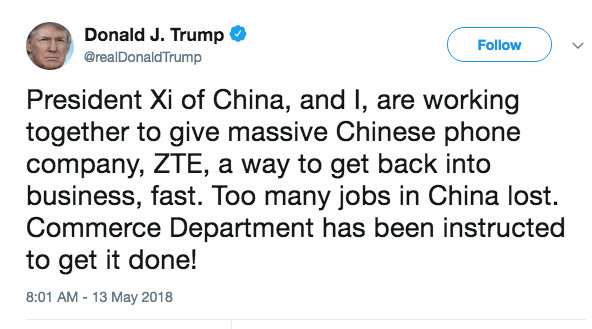

The U.S. Department of Commerce's Bureau of Industry and Security (BIS) agreed to temporarily lift export restrictions to ZTE that ...

Cincinnati Bell completed its acquisition of Hawaiian Telcom, the leading integrated communications provider serving Hawaiʻi, and the state’s fiber-centric technology ...

In a tweet on Sunday morning, President Trump said he has instructed the Department of Commerce to find a way ...

Equinix and Telxius, Telefónica's infrastructure subsidiary, are collaborating on U.S. facilities and services for the next-generation cable landing station architecture ...

A private dossier for networking and telecoms