Nokia wins 5G contract with Zain Saudi Arabia

Nokia announced a three-year deal with Zain Saudi Arabia to supply thousands of 5G sites across the country. Financial terms ...

Nokia announced a three-year deal with Zain Saudi Arabia to supply thousands of 5G sites across the country. Financial terms ...

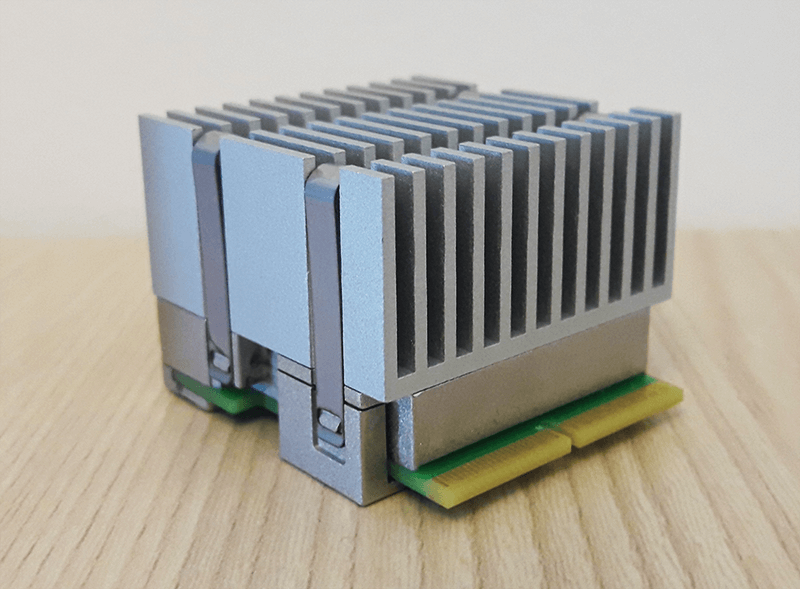

The world’s first optical modules compliant with Consortium for On-Board Optics (COBO) will be shown at next week's ECOC Exhibition ...

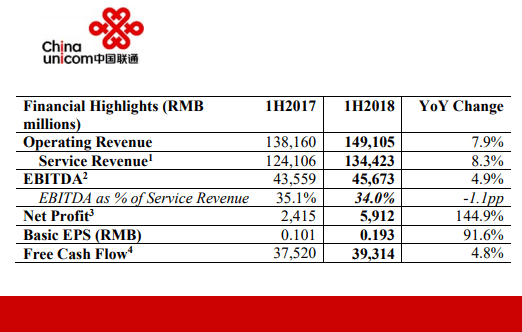

China Unicom reported 1H2018 service revenue of to RMB134.4 billion, representing an 8.3% year-on-year growth, topping rivals China Mobile and ...

A private dossier for networking and telecoms