ECOC 2018: First COBO-compliant optical modules

The world’s first optical modules compliant with Consortium for On-Board Optics (COBO) will be shown at next week's ECOC Exhibition ...

The world’s first optical modules compliant with Consortium for On-Board Optics (COBO) will be shown at next week's ECOC Exhibition ...

Cincinnati Bell completed its acquisition of Hawaiian Telcom, the leading integrated communications provider serving Hawaiʻi, and the state’s fiber-centric technology ...

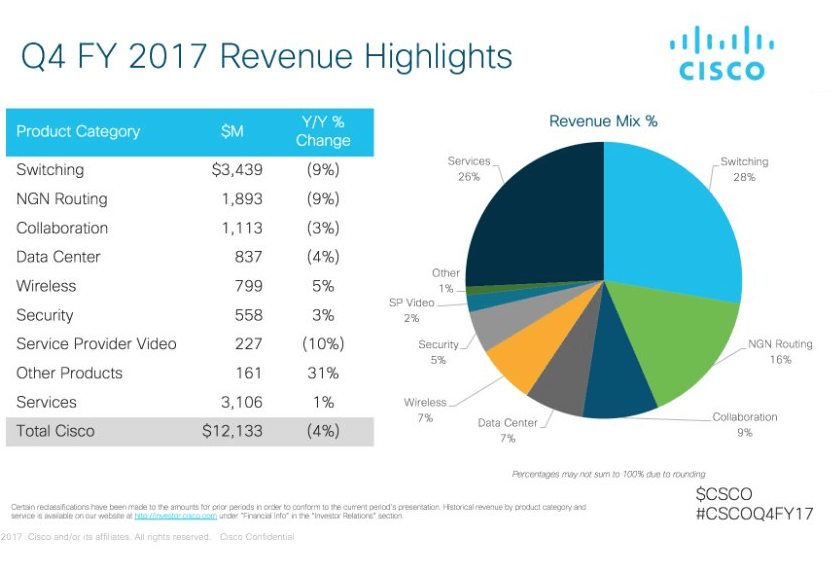

Cisco reported fourth quarter revenue of $12.1 billion, down 4% from $12.6 billion from the same time last year. Net ...

by James E. Carroll SK Telecom has developed a 5G repeater that improves signals in blanket/shadow areas by amplifying 5G ...

AT&T agreed to acquire Vyatta® network operating system and associated assets of Brocade Communications Systems. Financial terms were not disclosed. ...

A private dossier for networking and telecoms